Markets, Momentum, and Misconceptions

JACK JAMES - Sep 19, 2025

As we turn the page on summer, markets have continued to build on the strength that began back in April -strength that has caught many off guard, especially against a backdrop of confusing trade headlines, tariff chatter, and lingering worries from the last four years. That recency bias has left many skeptical of this rally, even as the data tells a different story.

.png)

Unemployment trends are a good example. Yes, there are signs of labour market cooling, but unemployment levels remain well below long-term averages. To us, this looks more like a normalization after years of pandemic distortion than the start of something more concerning. In the U.S., growth has been firmer; in Canada, softer - but taken together, the macro backdrop is hardly falling apart. If anything, the recent turn higher in leading economic indicators suggests green shoots may be on the horizon.

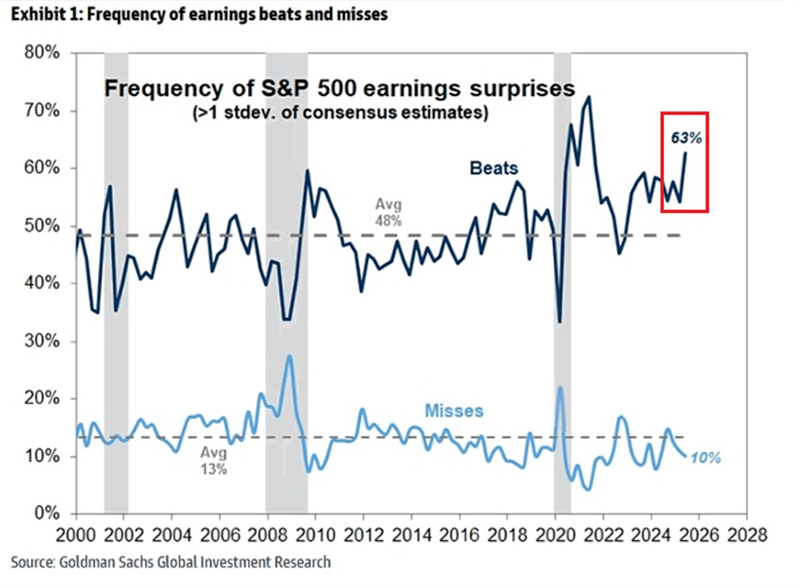

More importantly, when we look at the micro level - corporate earnings - the picture is very different from the cautious headlines. This past quarter delivered one of the strongest earnings “beat rates” in decades, with margins holding firm and forward guidance climbing. Companies are proving resilient, and in many cases, profitability is not just intact but improving. For us, this is the signal that matters most: earnings power, not economic noise, ultimately drives markets.

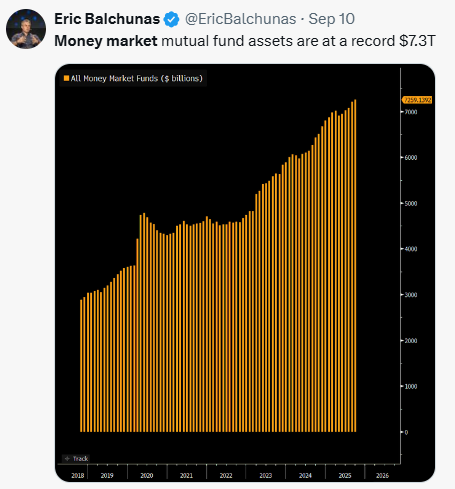

Layered on top of this is a meaningful policy shift. Both the Bank of Canada and the Fed have reignited their easing cycles with two recent quarter point cuts. Beyond simply adding liquidity, rate cuts are helping to relieve one of the stickiest elements of inflation - mortgage interest costs. If this also helps unstick real estate activity, it should buffer weaker areas of the economy and add to overall momentum. History also suggests that cutting rates near market highs is not a negative - if anything, it has often extended rallies. And with over $7 trillion still parked in U.S. money market funds, lower yields could nudge that cash back into risk assets - another potential tailwind for equities.

And then there is AI, which continues to sit at the center of the structural story. Record investment is flowing into infrastructure, automation, and innovation, already showing up in corporate earnings. But in our view, this theme is still very early - misunderstood and doubted, much like the early days of the tech, media, and telecom breakout of the 2010s. The longer-term implications for productivity, profitability, and innovation remain immense.

All of this adds up to what has become one of the most doubted rallies in memory. Much like the early years of the post-2008 cycle, skepticism remains high even as fundamentals improve. Strength without froth is not something we worry about - in fact, it reinforces our conviction as we head into the fall.

- Jack

The Smartest Way to Save for Your First Home:

Are you or someone you know planning to buy a first home? The Tax-Free First Home Savings Account (FHSA) is a powerful way for first-time buyers to save up to $40,000 - tax-free - toward a qualifying home purchase.

The FHSA combines the best features of RRSPs and TFSAs, offering:

- Annual contributions of up to $8,000 (lifetime maximum of $40,000)

- Tax-deductible contributions

- Tax-free growth on investments held within the account

- Tax-free withdrawals when used to buy a qualifying home

Explore our newest animated video in the Your Money Journey series. This short, engaging video explains how the FHSA works, who can benefit, and how it fits into a first-time home buyer’s financial plan

Don’t Miss Year-End Deadlines:

As we head into the final stretch of the year, it’s a good time to review a few key planning items:

-

RESP Contributions – To maximize government grants, contributions must be made before December 31st. Even a partial contribution can capture matching dollars.

-

TFSA Top-Ups - The 2025 limit is $7,000 per individual. If you haven’t fully used this year’s room, adding before year-end means more time for your investments to grow tax-free.

-

FHSA Contributions - The annual limit is $8,000 (with a lifetime maximum of $40,000). Contributions made before December 31st count toward your 2025 tax year, and unused room can carry forward.

-

Charitable Giving - Donations made before December 31st qualify for 2025 tax credits. Donor-advised funds can simplify larger gifts while giving flexibility over timing.

It’s worth reviewing these before the holiday season sneaks up. If any of these apply to you, please reach out to one of our team and we’ll make sure the right moves are in place.

Stablecoins: A ChatGPT Moment for the Blockchain?

Stablecoins are quickly emerging as one of crypto’s most practical applications. Pegged to traditional currencies like the U.S. dollar, they’re already streamlining everything from currency trades to global payroll - delivering fast, low-cost transactions with 24/7 settlement across borders.

Much of this innovation is happening on the Ethereum blockchain, the platform behind smart contracts and, in our view, the most likely foundation for tomorrow’s financial infrastructure. As adoption grows and regulation catches up, stablecoins are becoming a key pillar of digital finance. A recent Yahoo Finance article highlights Ethereum’s central role in this shift and reinforces our long-standing investment focus on tokenization - the digital representation of real-world assets.

For a quick primer on stablecoins, here’s a great resource: