The Wall, The Worries, and The Winners

Jack James - Jun 04, 2026

Markets climbed through a long list of worries to start the year. The reason why comes back to one thing: earnings are finally catching up to the hype

The first half of the year has been a useful reminder that markets rarely wait for a clean, comfortable backdrop before moving higher. We began the year with a long list of concerns - geopolitical conflict, oil market risk, inflation anxiety, central bank uncertainty, and growing debate over whether artificial intelligence enthusiasm had pushed markets too far, too fast. Many of those concerns remain unresolved today, yet equity markets have continued to climb the wall of worry.

.png)

The reason, increasingly, comes back to earnings. For much of the past two years, the artificial intelligence story has been framed around spending. Investors have watched some of the world's largest companies commit enormous sums to data centres, chips, power infrastructure, networking equipment, and software development, while questioning whether the eventual returns would justify the investment. Rather than slowing, those investments continue to grow, with many of the largest technology companies raising spending plans as demand for AI infrastructure continues to exceed available supply.

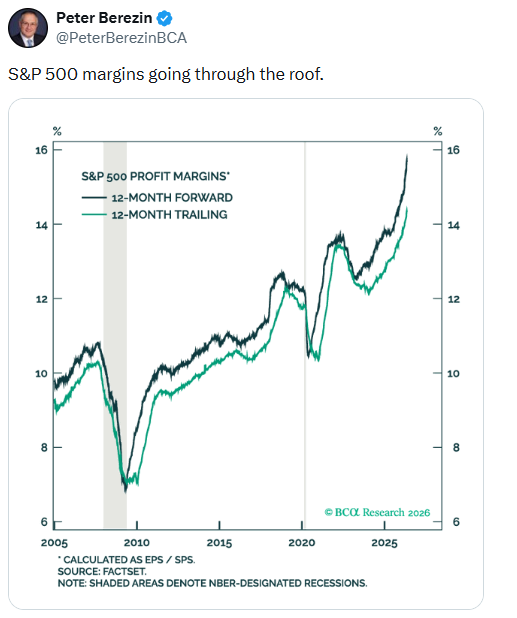

What has changed in recent months is that the AI buildout is no longer just showing up as spending. It is increasingly showing up in sales growth, margin expansion, and earnings expectations. S&P 500 profit margins are pushing toward multi-decade highs:

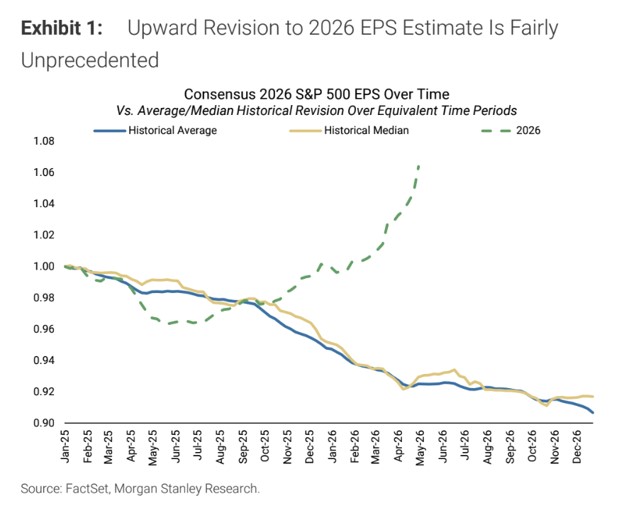

Forward earnings estimates continue to rise:

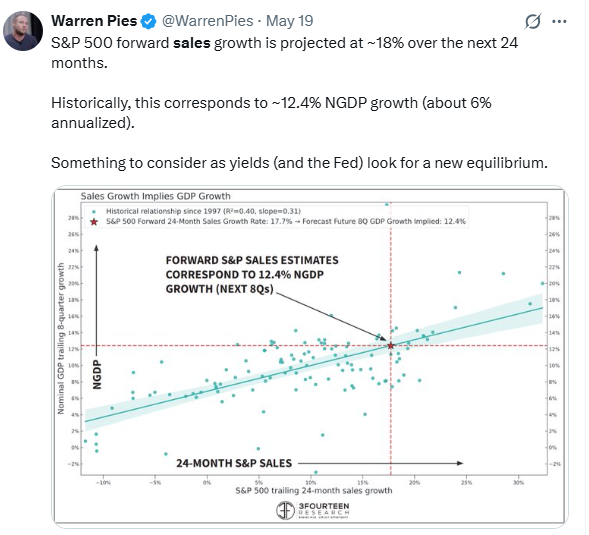

And projected sales growth remains unusually strong:

That does not mean there are no pockets of froth within the market, particularly around some of the more speculative corners of the AI ecosystem. However, it does help explain why we continue to view many of the broad bubble comparisons as misplaced. Increasingly, the spending is being matched by real revenues, expanding margins, and improving earnings, which is precisely what one would hope to see if the underlying opportunity is genuine.

Closer to home, the story feels more complicated. Canada’s economic backdrop has weakened meaningfully this year, with recent GDP data confirming that growth has stalled and the economy has contracted for two consecutive quarters, meeting the definition of a technical recession. Slower activity, price pressure on consumers, and a housing market still digesting the impact of higher rates have all contributed to that backdrop. For Canadian investors, that can create an understandable disconnect. If the economy feels weak, why are Canadian markets still moving higher?

Part of the answer is that the stock market is not the economy. Markets are forward-looking and constantly trying to price in what conditions may look like six, twelve, or even eighteen months from now. Economic data, by contrast, often tells us where we have already been. That is why recessions can feel confusing from an investment perspective. By the time a technical recession is officially identified, markets have often spent months assessing the slowdown and may already be looking ahead to the eventual recovery. While we believe diversification remains important for navigating these periods, it is also a reminder that weak economic headlines do not necessarily translate into weak market returns.

As we head into the summer, another sign of improving investor confidence is the renewed buzz around IPOs. Companies such as OpenAI (ChatGPT), Anthropic (Claude), and SpaceX are already being valued at extraordinary levels in private markets, with many investors believing each could eventually be worth trillions. SpaceX is expected to IPO in the not-too-distant future, while Anthropic may not be far behind. Whether the sky-high IPO valuations being suggested today ultimately prove justified remains to be seen, but the renewed enthusiasm itself tells us something. Earlier in the year, investors were focused on what could go wrong. Today, they are once again willing to look ahead and fund ambitious growth stories.

For now, we remain more comfortable participating in these IPOs indirectly through several of our core model holdings that are already deeply embedded in the AI ecosystem. Microsoft is estimated to own approximately 27% of OpenAI's for-profit business, while Alphabet (Google) holds an estimated 14% stake in Anthropic and roughly 7% of SpaceX. Amazon is also estimated to own approximately 14% of Anthropic. Nvidia has taken strategic positions across parts of the AI ecosystem while supplying much of the underlying infrastructure that powers it. While these ownership stakes are only estimates and continue to evolve as private companies raise capital, they provide our portfolios with meaningful exposure to many of the same long-term themes, without needing to underwrite private market valuations that may or may not already reflect a great deal of future success.

As we head into the summer months, there is certainly no shortage of things for investors to worry about. The difference today is that many of those concerns are increasingly competing with a backdrop of improving earnings, expanding margins, and continued investment in what may prove to be one of the most significant technology investment super cycles of our lifetimes.

There will undoubtedly be further bouts of volatility along the way, and markets will continue to debate the pace, scale, and ultimate impact of these investments. For now, however, the story continues to unfold much as it has over the past two years - one quarter, one earnings season, and one investment announcement at a time.

- Jack

Purpose Behind the Advice

In this interview with Michèle Soregaroli on Differentiation with Michèle, I had the opportunity to share more about my personal journey, the experiences that shaped my approach to wealth management, and why helping families have meaningful conversations about wealth, legacy, and intention is so important to me.

We explored how my family story, my early curiosity about financial planning, and my work in tax, estate, philanthropy, and intergenerational planning have influenced the way I serve clients today. For me, wealth management is not only about investments, tax strategies, or estate plans. It is about understanding the people, values, relationships, and responsibilities behind the numbers, and helping families plan with greater intention for the generations to come.

I hope this conversation gives you a more personal look at who I am, why I do this work, and the purpose behind the advice we provide.

- Alysha

Greater Transparency Around Investment Costs: What to Know About CRM3

Beginning in 2027, Canadian investors will receive enhanced investment cost disclosure through new CRM3 reporting requirements. These changes will provide a more complete picture of the costs associated with investment products, including fees embedded within mutual funds and ETFs.

While transparency is always welcome, cost is only one factor when evaluating an investment strategy. Portfolio construction, financial planning, tax strategy, risk management, and ongoing advice remain equally important considerations.

For a detailed overview of CRM3, Total Cost Reporting, and what these changes mean for your investments, click here to learn more.

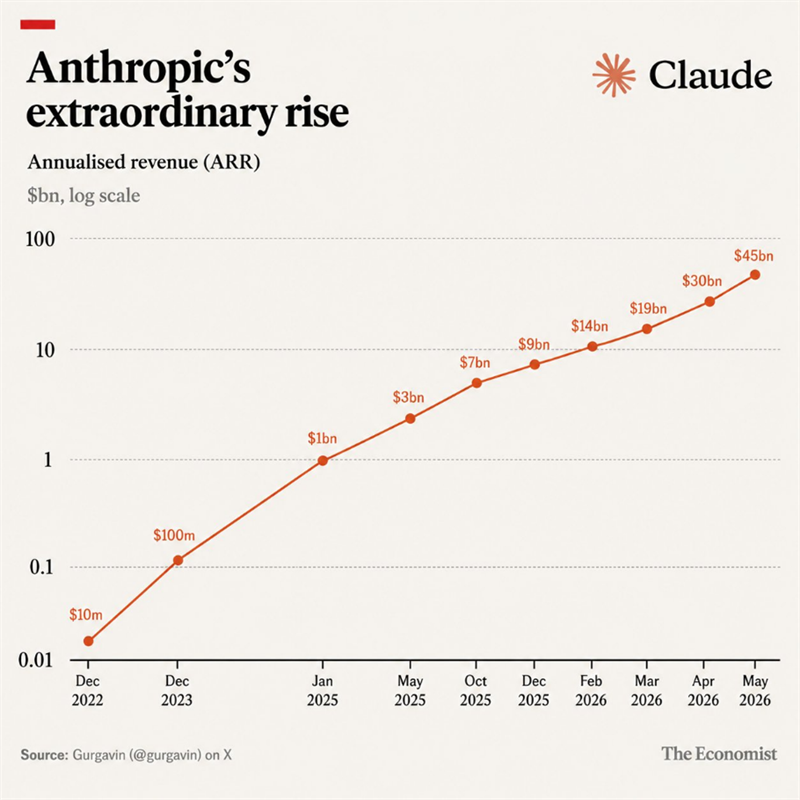

Anthropic's Extraordinary Rise and why it should be appreciated

By now, many of you have heard of Anthropic and its AI model, Claude. While ChatGPT captured much of the early consumer attention, Anthropic has quietly built what can only be described as one of the most remarkable growth stories in technology history.

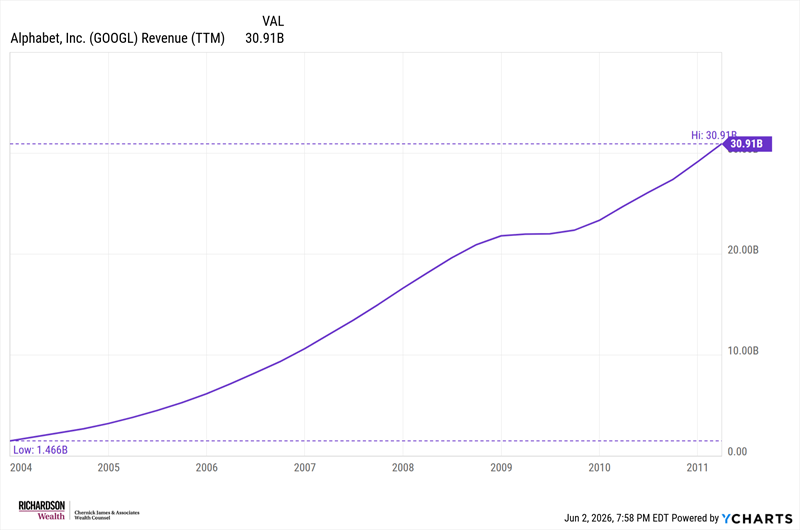

Its strategy has been surprisingly simple: focus on enterprise customers, where the economic value of AI is ultimately created, and lean into coding - an area where Claude has demonstrated a clear edge and which many believe sits at the heart of the path toward Artificial General Intelligence. The results have been staggering. As the accompanying chart shows, Anthropic's annualized revenue grew from roughly $1 billion to $30 billion in just 15 months, a figure publicly confirmed by management. More recent estimates place annualized revenue north of $45 billion.

We've followed technology companies for a long time and have seen some extraordinary growth stories. Yet nothing quite resembles what Anthropic has accomplished. It took Google roughly seven to eight years to reach US$30 billion in annual revenue. Anthropic's annualized revenue run rate reportedly surpassed that level in less than 15 months. The comparison is not perfect, and it is reasonable to expect the current growth rate will moderate over time, but the order of magnitude difference in growth speed is difficult to ignore.

Beyond the impressive numbers, this serves as a useful reminder that despite persistent claims that AI lacks a clear return on investment, the evidence increasingly suggests otherwise. While much of the public conversation remains focused on AI's costs, companies like Anthropic are demonstrating that for many enterprises, the value proposition is already proving very real.