Confusion as the Steady State

Jack James - May 01, 2026

Markets have begun to move on from last month’s surge in uncertainty, even as the situation remains unresolved. A familiar pattern - where volatility reflects shifting narratives more than changing fundamentals, and where a steady hand matters most.

There are a number of things that make investing difficult, but one of the most consistent challenges is deciding what to do with the constant flow of information. Markets are shaped by a steady stream of headlines, data points, and narratives, many of which can feel urgent and actionable in the moment. The difficulty isn’t a lack of information, but knowing when to respond to it and when to step back and let it pass.

That dynamic has been on full display over the first half of the 2020s, as we’ve moved through a steady stream of events that, in real time, have felt significant enough to challenge long-held assumptions - only to see markets ultimately push forward. It reinforces a point we continue to come back to: volatility is not an anomaly. It is the price of admission, and a feature of markets rather than a flaw. As a result, a steady hand and long-term mindset are as important as ever, if not more so today.

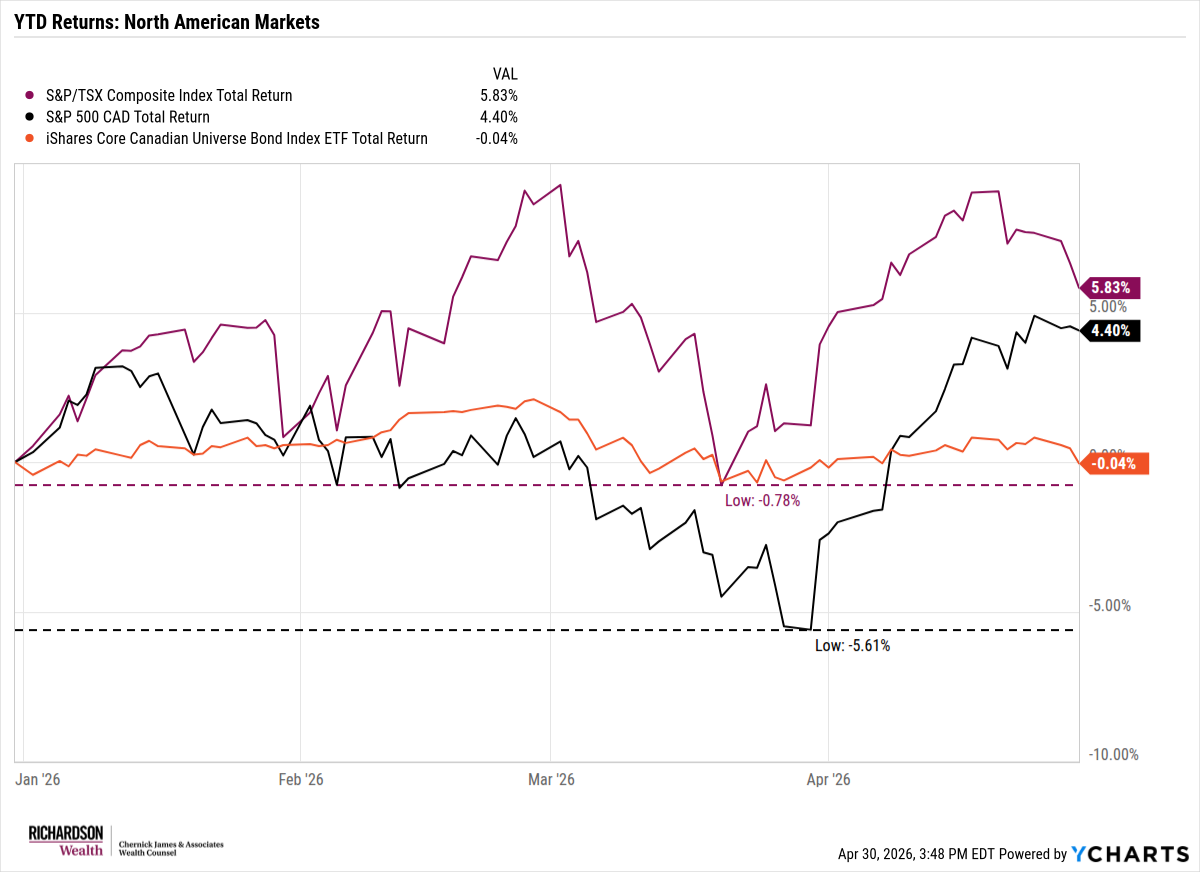

As we wrote about last month, we saw this play out again as markets worked through a surge in uncertainty tied to developments in the Middle East. At the time, the range of possible outcomes was wide, and markets were reacting accordingly - attempting to price in everything from contained conflict to a more disruptive escalation. Fast forward a month, and while the situation itself remains in limbo, signs of de-escalation have been enough to shift sentiment. Both U.S. and Canadian equities have recovered from their lows and are now back into positive territory on the year:

That raises a natural question: why would markets move higher when the underlying issue has yet to be fully resolved? The answer, in many ways, lies in how markets themselves work. Markets don’t wait for full clarity. They adjust as uncertainty is introduced, and just as quickly begin adjusting again as that uncertainty starts to narrow. In this case, while the conflict remains unresolved, some of the more extreme outcomes have, at least for now, been taken off the table. The initial shock - particularly around the risk of more sustained disruption to energy markets - has been absorbed.

Oil, which was at the center of much of the initial market reaction, moved sharply higher as those risks were first being assessed. That move brought with it a wave of concern around inflation, central bank policy, and even recession risk. Since then, a more balanced picture has emerged. Supply has proven more resilient than initially feared, alternative routes have absorbed some of the pressure, and the worst-case assumptions around a full disruption have not materialized.

The result is not a market that has ignored the risk, but one that has recalibrated it. This is an important distinction, and one that connects directly back to the broader theme we’ve been highlighting. Markets are constantly processing new information, often faster than it can be fully understood. What feels unresolved from a headline perspective can already be partially reflected in prices. In that sense, what we are experiencing is less a temporary phase of uncertainty, and more a steady state. One where multiple narratives - geopolitical, economic, and technological - are all unfolding at once, each with their own set of unknowns. And there is no shortage of those as we look ahead.

The U.S. midterm elections later this year will inevitably introduce another layer of volatility, as they tend to do. We are also seeing a transition at the Federal Reserve, with a new chair stepping in at a time where the path for monetary policy remains highly debated. Closer to home, the upcoming review of USMCA has the potential to create additional friction for both Canadian and U.S. markets. And underpinning all of this is the ongoing evolution of artificial intelligence - where the magnitude of investment, the pace of development, and the long-term implications continue to drive both optimism and skepticism in equal measure. Each of these will, at various points, take their turn driving headlines and influencing sentiment. They will feel important in the moment, and will likely contribute to periods of volatility along the way.

But if the past several years have shown us anything, it’s that markets are capable of absorbing a great deal of uncertainty while still moving forward. Not in a straight line, and not without disruption, but forward nonetheless. Our role through all of this remains the same: to stay grounded in the underlying fundamentals of the businesses we own, to adapt as conditions evolve without becoming reactive to every shift in narrative, and to maintain the discipline required to navigate environments where clarity is often limited. There will always be another headline, another risk, another reason for markets to pause. That is not something to be solved - it is something to be managed. And in that environment, a measured approach and a long-term mindset remain the most reliable tools we have.

As always, we will continue to monitor developments closely and position portfolios accordingly as the year unfolds.

- Jack

Ternus Time – A New Era at Apple

The recently announced leadership transition at Apple is a story worth paying attention to. For many, including our clients, Apple has been more than just a core holding - it’s been a defining story of modern markets. I still remember watching the original iPhone announcement from Steve Jobs at my desk as a young institutional analyst. At the time, it felt important. In hindsight, it reshaped not just a company, but an entire ecosystem..

What followed under Tim Cook was different, but no less remarkable. Cook doesn’t always get the credit he deserves. He wasn’t the visionary product storyteller that Jobs was, which has led to a narrative that innovation slowed under his leadership. But that misses the bigger picture. Apple became one of the most operationally dominant companies in history. AirPods, Apple Watch, Services, Apple TV+, and Apple Silicon weren’t accidents - they expanded the ecosystem, deepened customer loyalty, and drove one of the most significant increases in shareholder value we’ve seen. Apple’s market capitalization grew from roughly ~$350 billion when Cook took over to nearly $4 trillion at its peak. That’s not a lack of innovation - it’s execution at scale.

Today, Apple finds itself at a different kind of inflection point. The company has faced growing criticism for not moving quickly enough on artificial intelligence. While others have been more aggressive, Apple has taken a more measured approach. Its chips have quietly positioned the company well, particularly for running AI directly on devices, which could prove more important than it appears today. Still, perception matters, and for a growing number, the perception is that Apple is falling behind.

That sets the stage for John Ternus, who is set to take over from Cook later this year. Ternus steps in not as an operator in the mould of Cook, but as a product engineer - closer to the DNA that originally defined Apple. The question now is whether this marks a shift back toward bold product innovation, or simply an evolution of what has already been a highly successful model. Can Apple reassert itself at the forefront of new categories - whether AI, robotics, healthcare, or something not yet fully imagined? Those are big questions, and they won’t be answered overnight.

What we do know is this: Apple has earned the benefit of the doubt. Few companies have navigated multiple technological transitions as successfully, built ecosystems as durable, or have the scale to pivot when the time comes. As the next chapter begins, it will be worth watching closely, because Apple tends to move deliberately, and when it does, it tends to matter.

Longevity, AI, and the Next Frontier

When we talk about artificial intelligence, most of the focus tends to be on productivity, automation, and disruption. One area that gets far less attention, but may ultimately be just as impactful, is how it’s beginning to change the way we approach human health and aging.

Longevity science is an emerging field focused on understanding how we age and how to extend not just lifespan, but the number of healthy years we live. It’s still early, but progress is picking up quickly, in large part because AI is helping researchers test ideas, analyze data, and develop new therapies much faster than before.

I recently came across a conversation from the Abundance360 Summit featuring David Sinclair, a Harvard Medical School professor and one of the leading researchers in this space. He discusses some of the latest developments, including how advances like epigenetic reprogramming may begin to change how we think about aging over time.

If you’d like to hear more about their work in longevity science, I’d encourage you to watch the video below.